Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkTourism & Management Studies

versão impressa ISSN 2182-8458

TMStudies no.7 Faro dez. 2011

The New Challenges of Tourism Airports -The Case of Faro Airport

Os novos desafios dos aeroportos turísticos – o caso do aeroporto de Faro

Cláudia Ribeiro de Almeida

Adjunt Professor, University of Algarve – ESGHT calmeida@ualg.pt

ABSTRACT

Airport infrastructures play an important role in the heart of the regions in which they are located, as well as in certain sectors of activity, such as tourism. In recent years, their positioning has been altered from a passive attitude to an active attitude due to new market demands and new trends which have arisen in associated sectors, such as the air transport sector.

The 1997 deregulation of air transport in Europe led to major changes on the way people travel. One of the most interesting results of deregulation, was caused by the fact that the low cost airlines appeared on the market with a business model distinct from the traditional scheduled and charter airlines, allowing for the opening up of new airports and new tourist destinations. Those airlines are also responsible for some of the main changes in the airports operations and market positioning.

The increase in routes and frequencies offered by these airlines enabled the emergence of new tourist destinations in Europe that spread, later on, to other places all over the world. The ease of purchasing an airline ticket online, and the availability of attractive routes at affordable prices allowed the development of new market segments, such as second home tourism. One of the main impacts of low cost operations has been the changing of airport's structures, mainly to the ones that traditionally received charter flights. In this article we are going to explore the case study of Faro airport, an excellent example of this changes.

KEYWORDS: Airports; Tourism airports; Faro Airport

RESUMO

As infra-estruturas aeroportuárias desempenham um papel importante nas regiões onde se inserem, bem como em determinados sectores de actividade, como o turismo. Nos últimos anos, o posicionamento destas infra-estruturas passou de uma atitude passiva para uma atitude mais activa, devido a novas tendências de mercado que têm originado um novo posicionamento e uma nova dinâmica de actividades. O processo de desregulamentação, que ficou concluído na Europa em 1997, originou grandes alterações no sector do transporte aéreo, permitindo a entrada no mercado das companhias aéreas de baixo custo e por consequência uma alteração no sector aeroportuário, uma vez que apresentam características distintas das companhias aéreas regulares tradicionais ou de bandeira, assim como das companhias aéreas charter. O aumento de rotas e frequências oferecido pelas companhias aéreas de baixo custo permitiu o desenvolvimento de novos destinos turísticos um pouco por toda a Europa. A facilidade de reserva, aliada a tarifas atractivas para diversas rotas, permitiu o desenvolvimento de novos segmentos de mercado, como por exemplo o turismo residencial. Um dos principais impactes da entrada destas companhias aéreas no mercado foi a alteração que originou nas estruturas de tráfego dos aeroportos para onde operam, principalmente os que acolhiam tradicionalmente voos de companhias charter. Neste artigo será explorado o caso do Aeroporto de Faro, um exemplo excelente, uma vez que conheceu várias alterações devido ao início da operação das companhias aéreas de baixo custo.

PALAVRAS-CHAVE: Aeroportos, Aeroportos Turísticos, Aeroporto de Faro.

INTRODUCTION

During recent years airports have been changing their strategies and positioning in order to go forward to meet new market challenges, increasingly demanding and competitive.

The market entry of low cost airlines resulted in changes in the structure of air traffic from various European airports, particularly those associated with an operation dictated by seasonal charter flights, in many cases in tourist destinations.

Faro Airport is one such example, showing until mid-1990 a seasonal operation essentially based on charter flights (more than 80% of passengers). Since the entry of low cost airlines and due to the rapid rise in demand from passengers, the airport has seen a dramatic change in their traffic structure, with about 75% of passengers handled in 2010 by the low cost airlines.

The main objective of this article is to discuss some theoretical considerations about tourism airports and in the case study to present some actual data about Faro Airport in the south of Portugal, which shows the main changes in traffic structure. The main objective of the case study is to discuss the implications that all of those traffic structures had in the Faro Airport operations and in the main infra-structures.

1. EVOLUTION OF CONCEPT AND THE AIRPORT BUSINESS

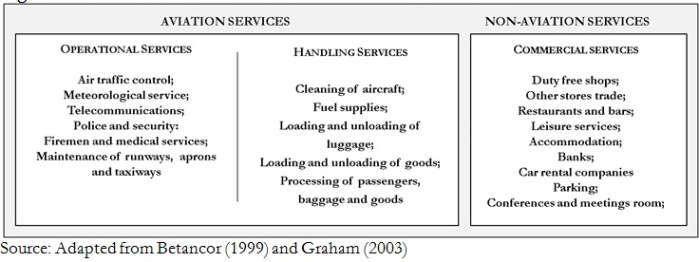

An airport can be defined as a system that serves a variety of needs related to the movement of goods and passengers, representing an essential component of the air transport system. Betancor (1999) and Graham (2003) point out that an airport is composed of infrastructures to support the processing of aircraft, passengers and cargo, such as one or more runways, aircraft parking apron areas, roads, passenger terminal and cargo terminal, and a control tower, among others.

Each of these components serves different purposes which, when combined, allow an interchange between overland and airborne means of transport (Betancor, 1999; TRL, 2006 in European Parliament, 2007).

The concept of an airport has evolved in recent decades. It is no longer seen only as a physical infrastructure which gives a modal transfer (of passengers and cargo) between ground and air (Ashford, 1985). Today it is an intermodal transportation centre geared towards development, a platform for various commercial activities and a partner for economic development (ACI, 2006).

Activities that may exist in an airport are classified by Betancor (1999) and Graham (2003) as: (i) Operational services; (ii) Handling services; (iii) Commercial activities (Figure 1).

Figure 1: Classification of Aviation and Non-Aviation Services

Pertaining to demand, an airport does not have a direct demand, but one that is derived from the fact that it is related to socio-economic activities of the population, and indirect, as is it generated by airlines, a situation which restricts the entire airport business.

2. THE NEW POSITIONING OF AIRPORTS

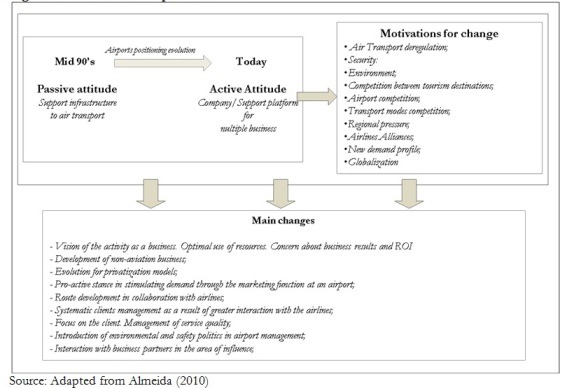

In the last two decades, the airport sector has been affected by issues of a social, political, legal, economic, technological and environmental nature that have led to changes in its positioning and business model (Figure 2).

Figure 2: Evolution of airport elements

The deregulation of air transport, issues related to safety and the environment, competition between destinations, between airports and between modes of transport, regional pressure, alliances between airlines, and the new profile of demand and globalisation have led to profound alterations and changes to the structures and business models of airports, which, when combined with concepts of strategy, innovation and quality, create a new strategic positioning with direct implications on the development of the regions under their influence (ARC, 2003).

The evolution and maturity of the sector have increased the need for commercial management and financial practices giving priority to the "marketing" of airports.

This type of airport "marketing" model is distinguished, according to Pita (2008), in different forms:

(i) Greater distance from the State, which gives it greater commercial and operational freedom, maximising the development of new businesses, partnerships and private investment;

(ii) Creation of airport companies with a more professional management model which focuses on commercial and financial components;

(iii) Importance of airport revenue, namely those from non-aviation activities which allow for the development of the business;

(iv) Development of airport marketing, which has created a proactive attitude in the development of air traffic, an improvement in external interfaces with clients, partners and other interested parties, and also the suitability of the quality of the service.

An airport is no longer just an infrastructure to support air transport. Today, it is seen as a centre for regional and national development which, together with other stakeholders, participates in the development strategies of the region, both in the tourism sector (regional and international) and other sectors of activity, allowing the destination to become more attractive and therefore more sought after by domestic and foreign investors. Its positioning allows it to delineate strategies of optimisation and maximisation of resources with a view to obtaining the best possible results and a fast and sustained return on investment (Graham, 2003). According to Suau (2007), airport planning is not a simple task because its business is influenced by different variables, with a global and uncontrollable character, together with other areas which exert pressure when it is time to decide and define strategies.

The development of non-aviation commercial activities, supported by the business component quickly became a source of revenue. Today, airports are now innovative and diversified commercial spaces in terms of the commercial brands, activities and services offered, allowing them to meet the new demand trends and to monitor the increasingly competitive and global market.

To address these new trends several airports are turning to private management models, which arise due to budgetary constraints inherent in the public sector, the need to expand infrastructures to keep up with growing demand and to introduce processes that are more innovative and suited to new market trends (Freathy, 1998). The pro-active position that airports have today allows them to meet demand and establish a closer and more dynamic relationship with the airlines in the development of routes and in the devising of strategies for joint promotions. Focusing on the client is one of the premises of the activity of airports, supported by measuring mechanisms for its performance through the implementation of service quality management systems which allow the constant monitoring of the various operating areas, and the updating and improvement of processes (Humphreys, 2002).

Regarding internal operational policies, there are the issues of quality, the environment and safety, important pillars for the sustainable development of these infrastructures and the entire surrounding region (Graham, 2003).

An airport competes with other airports, located in competing destinations and which present themselves to the market in an attractive manner and sometimes with similar products to its own. The changes associated with this type of competition give rise to a growing need for information pertaining to the market in which the airport operates, both in terms of the supply (the region's infrastructure, services, complementary supply, among others), and the tourism demand in the region (analysis of the behaviour, needs, profile, etc.).

This will allow each airport to tailor its strategies to market trends and act with other public and private participants within its area of operation, whether in attracting new flows of demand to the region, new contacts with airlines, the development of new routes, increased frequencies, or new investments and the consequent sustained and integrated development of the destination. The role of an airport is therefore more and more dynamic and is based on an integrated management of knowledge, shared and sustained with a view to achieving more and better deals for the entire area of action, reasons that enhance an increasing approximation of those infrastructures to public and private entities, namely research centres and universities, with a view to developing new platforms for the sharing and publishing of this information.

3. EVOLUTION OF AIRPORT RELATIONSHIPS WITH AIRLINES

The relationship between airport operators and airlines is critical to the success of any airport, so internal strategies and procedures that enable an easier and more effective negotiation have been developed so that they can work together.

In recent years the air transport industry has experienced less positive times, a consequence of adverse factors such as the incidents of the 11th of September 2001 in New York, the war in Iraq and the SARS epidemic in 2003 which led to a widespread economic recession with direct implications in several countries (Almeida et al, 2005; Almeida et al, 2006). The above mentioned incidents weakened both the air transport sector and the airport sector and delayed planned investments or the achieving of strategic partnerships, due to the risk involved (Graham, 2008).

The entry of low cost airlines into the market has led to new challenges for airports in order to be able to respond to their demands and needs, namely those relating to airport charges or other support services in the terminal and apron (handling). Airports compete against each other, so each has to provide better benefits and services to airlines, as well as indexes of high safety and environmental care (Graham, 2008).

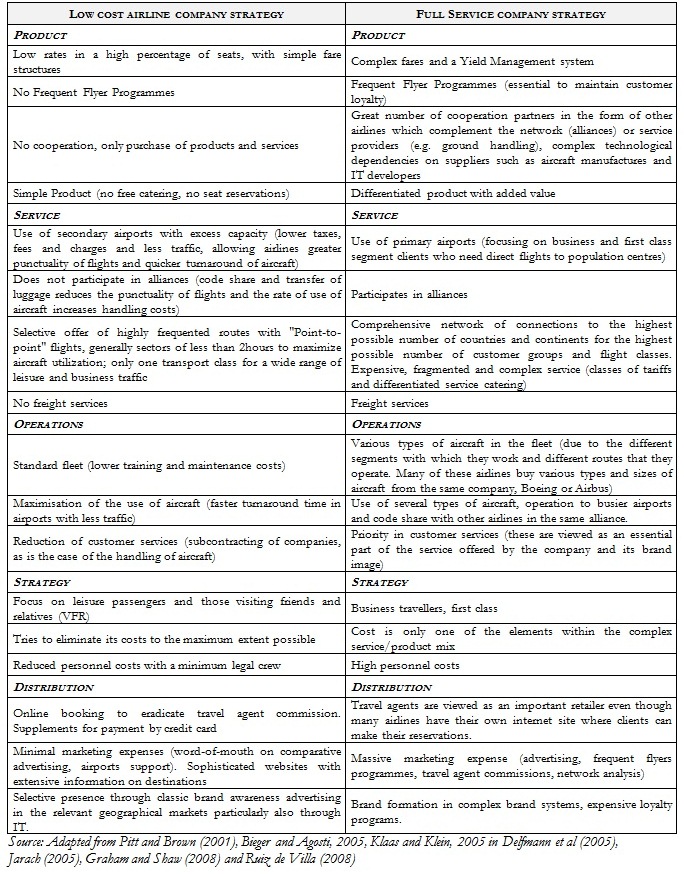

Pitt and Brown (2001) refer that the positioning of airports in order to satisfy the different types of airline has given rise to operational changes in requirements relating to the desired services and in the way the airports negotiate with these same airlines. To understand these differences in the services required we present a resume of the main characteristics of a low cost airline and a full service airline strategies proposed by Pitt and Brown (2001), Bieger and Agosti, 2005, Klaas and Klein, 2005 in Delfmann et al (2005), Jarach (2005), Graham and Shaw (2008) and Ruiz de Villa (2008) (see Table 1).

Table 1: Differences between the strategies of low cost airlines and traditional scheduled airlines

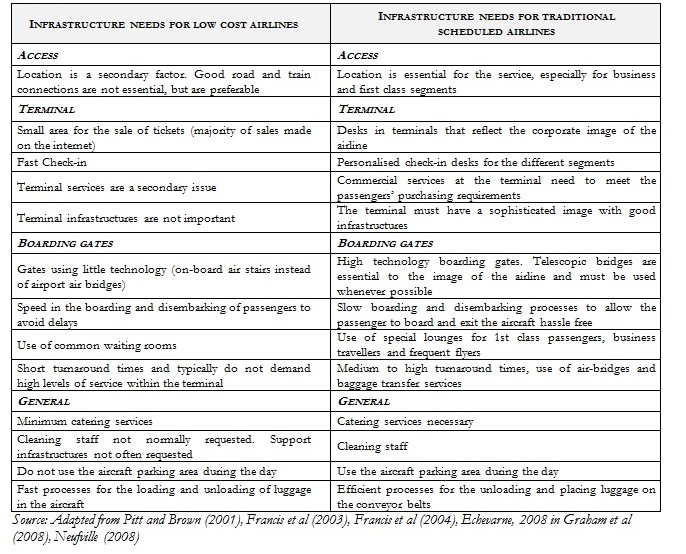

Pitt and Brown (2001), Francis et al (2003), Echevarne, 2008 in Graham et al (2008) and Neufville (2008) refers that the airlines have different needs concerning the airport service, a new challenge for these infrastructures which has resulted in changes to processes and the services provided (See Table 2).

Table 2: Intrastructures needed in an airport for low cost airlines and traditional scheduled airlines

Neufville (2008) refers that the airport planning is shifting from the traditional pattern driven by long-term point forecasts, high standards, and established clients to that of recognizing great forecast uncertainty, many standards and changeable clients. This is a consequence of economic deregulation of aviation and the rise of low cost airlines. The requirements of a low cost airline differ from those of the traditional regular airlines.

Low cost carriers find airport services a major area where they can achieve economies to ensure that their low fares are profitable. In the case of airport entities, a widespread diffusion of the low cost formula requires that all main operational procedures are adapted to the new dominant market trend (Jarach, 2005). This same author points out that typically, low cost airlines are aggressive in all B2B negotiations. In the case of airports, these players look for economic subsidies to cover start-up costs, cheap handling, landing and park fees, plus a significant efficiency in ground operations that will permit short turnaround times. For instance, Ryanair, the European low-cost leader, requires from all of its partner airports a tight 25 minute turnaround time.

All of these requirements represent a great challenge to the airports as it evolves some new complex operations.

One of the european airport that has undergone major changes in its operational area due to the strong presence of low cost airlines is the Faro Airport (Portugal), which we will present below.

4. CASE STUDY: FARO AIRPORT (ALGARVE, PORTUGAL)

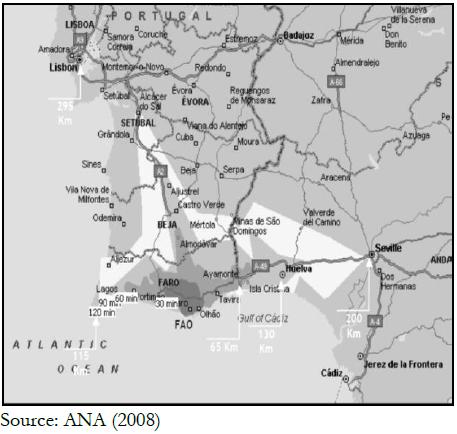

The National Airport System is comprised of various infrastructures, including airports, airfields, helipads and military bases (MOPTC, 2006). The existing airports in the mainland are located in Lisbon, Porto and Faro, as well as in the Madeira Islands (Madeira and Porto Santo) and the Azores (Ponta Delgada, Santa Maria, Horta and Flores). The company ANA Airports of Portugal, SA manages airports in the mainland and the Azores, while ANAM manages the island of Madeira (Map 1) (ANA, 2008).

Map 1: portuguease airports location

Our article focuses on the Faro Airport, which has as its main vocation international tourism traffic. According to Fonseca (2007) this airport has a catchment area of approximately 395,000 people

within 60 minutes, so if you add the area of Huelva (Spain) it amounts to 535,000 people. A

distance up to 180 minutes this figure may reach 1,286,360 people (Map 2).

Map 2: Faro Airport catchment area

The Huelva region is important for Faro Airport because it is a natural extension of its catchment area, creating incoming and outgoing traffic, which might be justified by the fact that the nearest Spanish airport is Seville (Fonseca, 2007).

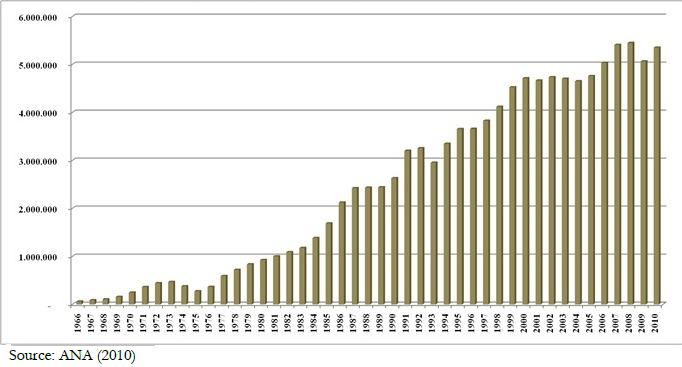

Faro Airport has presented over the four and half decades of operation, an increase in the number of passengers handled, accompanied by changes in its infrastructure in the early seventies, in the late eighties and in two thousand and one. These recent changes have allowed the increase of this airport capacity to six million passengers per year (Chart 1).

Chart 1: Evolution of passengers at Faro Airport (1966-2010)

All changes that have occurred in the terminal and other infrastructure allowed the airport to ensure a better level of service to airlines, passengers and other customers, enabling the development of traffic flow and consequently the tourism in the Algarve.

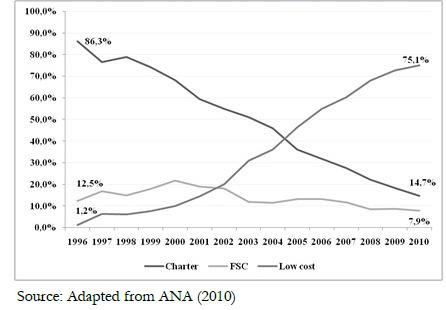

Since its opening, Faro Airport is mainly a tourism airport, with a charter and seasonal operation from the countries of Central and Northern Europe. From the mid nineties, and after completed the deregulation of air transport in Europe, the traffic structure has changed due to start-up of low cost airlines, which represented the end of 2010, over 75% of handled passengers (Chart 2).

Chart 2: Evolution of handled passengers at Faro Airport (1990-2010)

During the first decade of the 21st century Faro Airport has witnessed a complete change in the predominant transport model, with a decline in charter operations and the emergence of the low cost sector. This change took place on the supply side, i.e. essentially, airlines did little more than adapt the low cost model quickly and efficiently to the intrinsic structural characteristics of tourism in the Algarve in response to consumer demands (greater flexibility) and hence this did not result in a significant leap in the overall volume of visitors using this airport. Consequently, a more accelerated and sustained growth will fundamentally take place by stimulating an increase in demand, based on a diversification of markets as well as on innovation and differentiation and by promoting the tourism products that the region and its economic agents have to offer. The inauguration in March 2010 of the first operational base at Faro Airport by the largest and most aggressive European carrier in the low cost segment – Ryanair is now a enormous challenge for the mobilising capacity of regional economic agents.

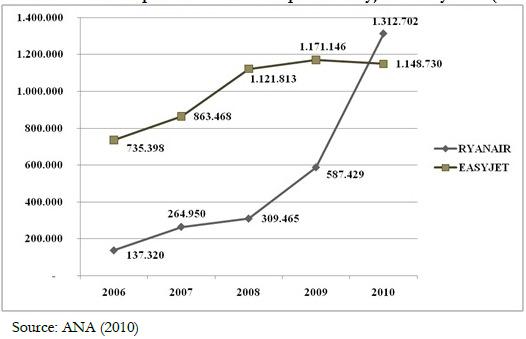

By the end of 2010 Ryanair reach the first position in passengers handled at Faro Airport with a growth of 123,5% compared to the previous year (1.392.702 passengers). By the same period Easyjet, the first one in the last years dropped for the second place, with less 1,9% passengers than in the previous year (1.148.730 passengers) (Chart 3).

Chart 3: Airline operation at Faro Airoirt - Easyjet and Ryanair (2010)

The operation of low cost airlines at Faro Airport led to the provision of new routes and flights to new regions of Europe throughout the year, allowing a significant improvement in the accessibility and development of new tourism market segments, as for example the residential tourism. This market segment is associated with people that travel abroad all over the year to stay in their second home. These clients appreciate the accessibility to the destination provided mainly by low cost airlines.

Europe was one of the regions that felt the impact of the economic crisis the most over the course of 2009 and 2010, especially in the tourism sector, where the United Kingdom is positioned as the largest market within the European Union supplying traffic to the Algarve. The United Kingdom, the dominant historical leader accounting for almost 54% of traffic to the Algarve dropped below the figure of 3 million passengers transported in 2010 with a decline of 3,4% of passengers transported (ANA, 2010).

Amongst the main markets, Germany was one of the least affected, with a positive variation of 12,9% passengers handled compared to 2009. The Dutch market also grown for about 13% compared with 2009 as a result of more connections to Faro. The Irish market saw a little drop of 0,4% which can be explained by the economic scenario in the country during the last years. Finally, the domestic market also recorded a growth during the past year (+5.3%). Two factors contributed essentially towards this exceptional situation: the consolidation of TAP traffic in Lisbon hub and, on the other hand, the effect of the direct Ryanair’s Porto-Faro connection, which was inaugurated in October 2009 (ANA, 2009 and 2010).

Keeping in mind the significant decline in airport activity, the traffic structure continued the trend observed in recent years, with the growth of the scheduled segment, which comprised 78% of traffic in 2009 and 85% in 2010, in the overall structure of passenger traffic according to the type of operation. This increase in the percentage of the scheduled segment was due to the growth in low cost operations as compared to the charter segment, which declined by 788.932 passengers transported (97.000 fewer passengers than in the previous year) and, on the other hand, to the scheduled operations of FSC (Full Service Carrier) airlines, with a 5,4% reduction compared to 2009. The low cost operations, which represent almost 90% of the scheduled segment, saw passenger numbers rise for about 21,6%, for a total of 4.020.214 passengers transported (ANA, 2009 and 2010).

In a year that witnessed a global slowdown in the international economy, where tourism was one of the most penalized activities, low cost airline companies proved to be the air transport segment that contributed the most towards a traffic growth of 21,6%. In contrast, as has been mentioned, traffic in the charter segment declined for the fifth consecutive year, recording some 788.932 passengers in 2010, which explains an annual average reduction of 15,3% over the course of this period. With a less pronounced decline, the scheduled FSC segment (FSC – Full Service Carrier) recorded about 421.364 passengers, about -5,4% than in the previous year (ANA, 2009).

With a view to suitably upgrading the infrastructure to be able to handle this new reality, ANA SA has already implemented a plan to develop Faro Airport, with a volume of investments of about 130 million Euros. This plan will focus on remodeling the facilities and increasing capacity to enable the airport to handle 8 million passengers by 2013.

CONCLUSIONS

This article assumes that airports now have a new positioning, resulting from factors that contributed to this infrastructure moving from a passive attitude to a more proactive one, with new approaches to the airlines, stakeholders and even in how they analyse the supply and demand of the various segments of the tourism market. These changes led to the need for updated information, important for devising strategies, proper negotiation with clients and a timely knowledge of market trends, supply and demand, competitors, and other factors.

This new positioning has raised the demand for specific data on certain segments of the tourism market, particularly those with implications on the structure of traffic and whose timely knowledge may change the way an airport structures the negotiation of routes with certain airlines.

An airport’s role is distinct from that of the other participants in the region in which it is located as it does not have direct demand, meaning that the client’s reason for going there is not to visit the airport, but because there is a particular underlying interest at the destination.

We can say that its current positioning involves a greater approximation to the market and a greater focus on factors that influence flows of demand throughout the year.

By being closer to the stakeholders of the destination and the airlines, an airport can work towards improved levels of service and the adoption of better strategies for attracting traffic.

At a time when the vulnerability of international markets is visible and has effects on tourism demand worldwide, it is essential that an airport looks out for social, political, economic, legal and even environmental signs because these may lead either to changes in internal processes or in traffic flows with direct implications for the airport business.

Knowledge is thus a powerful and very valuable weapon in this sense, as it can predict or anticipate changes in the demand or needs of specific market segments, allowing the most appropriate strategies to be taken in response to new challenges.

The case study presented reveals a great change in a Faro airport traffic structure, a tourism airport that has been changing all over the years to deal with the new tourism market trends and needs. From the mid nineties until today Faro airport knew a dramatic change in the traffic structure related to the entry of low cost airlines.

New challenges and strategies have been adopted to deal with this new airlines and passengers, i.e. in the operational point of view and in new investments in increasing capacity to handle 8 million passengers by 2013.

REFERENCES

ACI (2006): Understanding Airport Business. Airport Council International; [ Links ]

ALMEIDA, C. (2010): Aeroportos e Turismo Residencial. Do conhecimento às estratégias. Editorial Novembro, Coleccão Nexus; [ Links ]

ALMEIDA, C.; Ferreira, A. and Costa, C. (2005): "As companhias aèreas de baixo custo, pistas para possíveis investigações científicas", in VII Encontro Hispano-Luso de Economia Empresarial – Estratégia, Inovação e Desenvolvimento Sustentável no Turismo, Faro, 25 de Novembro de 2005; [ Links ]

ALMEIDA, C.; Ferreira, A. and Costa, C. (2006): "As companhias aèreas de baixo custo, uma realidade emergente no Algarve, um potencial tema de investigação", in 3º Congresso Nacional de Transportes do Grupo de Transportes da Faculdade de Economia da Universidade do Porto, Covilhã, 3 e 4 de Janeiro de 2006; [ Links ]

ANA, SA (2008): Faro Airport Presentation. ANA, Aeroportos de Portugal – Aeroporto de Faro, Fevereiro de 2008; [ Links ]

ANA, SA (2009): Annual Traffic Report 2009 – Faro Airport; [ Links ]

ANA, SA (2010): Boletim Mensal de Tráfego – Dezembro de 2010 – Aeroporto de Faro; [ Links ]

ARC (2003): "Airport Dynamics Towards Airport Systems", in Airport Regions Conference, Maio de 2003. Estudo da autoria de Jordi Garriga; [ Links ]

ASHFORD, N.; Stanton, H. and Moore, C. (1985): Airport Operations; McGraw-Hill; [ Links ]

BETANCOR, O. e Rendeiro, R. (1999): Policy Research Working Paper 2180: Regulating privatized infrastructures and airport services. World Bank Institute – Governance, Regulation and Finance, Setembro de 1999; [ Links ]

BIEGER, T. and Agosti, S. (2005) «Business models in the airline sector – evolution and perspectives», In DELFMANN, W; Baum, H.; Auerbach, S. and Albers, S (2005) Strategic Management in the Aviation Industry. Ashgate Publisher, pp. 41-64; [ Links ]

EUROPEAN PARLIAMENT (2007): The consequences of the growing European low-cost airline sector. Estudo realizado por uma equipa multidisciplinar da CESUR, Instituto Superior Técnico de Lisboa (Rosário Macário; Vasco Reis, José Viegas e Feliciana Monteiro) e do Department of Transport and Regional Economics (TPR), University of Antwerp, Belgium (Hilde Meersman, Eddy van de Voorde, Thierry Vanelslander, Peter Mackenzie-Williams e Henning Schmidt); [ Links ]

FONSECA, J.H. (2007): "Gestão de Aeroportos especializados no mercado turístico. Desenvolvimento de áreas de influência transfronteiriças", in Conferência Think’nomics 07, realizada no dia 18 de Junho de 2007, Lisboa;

FRANCIS, G.; Fidato, A. and Humphreys, I. (2003) « Airport–airline interaction: the impact of low-cost carriers on two European airports» In Journal of Air Transport Management, vol.9, pp.267– 273; [ Links ]

FREATHY, P. and O’Connell, F. (1998): "Supply chain relationships within airport retailing", in International Journal of Physical Distribution & Logistics Management, Vol. 28, nº 6, pp. 451-462;

GRAHAM, A. (2003): Managing airports – An international perspective. [2ª edição]. Elsevier Butterworth Heinemann; [ Links ]

GRAHAM, A. (2008) Managing airports – An international perspective. [3rd edition ]. Elsevier Butterworth Heinemann; [ Links ]

GRAHAM, B. and Shaw, J. (2008) «Low-cost airlines in Europe: Reconciling liberalization and sustainability» In Geoforum, vol.39, pp. 1439–1451; [ Links ]

HUMPHREYS, I. and Ison, S. (2002): "Ground access strategies: Lessons from UK airports?", in 82nd Annual Meeting of the TRB 2003. Committee on Airport Terminals and Ground Access A1J04; [ Links ]

ISIDRO CARMONA, A. (2010) Operaciones Aeroportuarias [2nd edition]. Fundación AENA; [ Links ]

JARACH, D. (2001): "The evolution of airport management practices: towards a multi-point, multiservice, marketing-driven", in Journal of Air Transport Management, vol. 7, pp.119 -125 [ Links ]

JARACH, D. (2004): "Future scenarios for the European Airline industry: a marketing-based perspective", in Journal of Air Transportation, vol. 9, nº 2, pp.23-39 [ Links ]

JARACH, D. (2005) Airport Marketing Strategies to cope with the new millennium environment. Ashgate Publisher; [ Links ]

KLAAS, T. and Klein, J. (2005) «Strategic airline positioning in the german low cost carriers (LCC) market», In DELFMANN, W; Baum, H.; Auerbach, S. and Albers, S (2005) Strategic Management in the Aviation Industry. Ashgate Publisher, pp. 119-142; [ Links ]

NEUFVILLE, R. (2008) «Low-Cost Airports for Low-Cost Airlines: Flexible Design to Manage the Risks» In Transportation Planning and Technology, February 2008, vol.31, nº1, pp.35-68. [on-line available] http://dx.doi.org/10.1080/03081060701835688

PITA, F. (2008): Marketing Aeroportuário. ANA, Aeroportos de Portugal – Aeroporto de Faro. Maio de 2008; [ Links ]

PITT, M. and Brown, A. (2001): "Developing a strategic direction for airports to enable the provision of services to both network and low-fare carriers", in Facilities, vol. 19, nº 1/2, 2001, pp. 52-60; [ Links ]

RUIZ DE VILLA, A. (2008) Los aeropuertos en el sistema de transporte. Fundación AENA; [ Links ]

STRAIR (2005): Air service development for regional development agencies. Strategy, best practice and results. STRAIR -Strategic development and cooperation between Airport Regions; [ Links ]

SUAU SÁNCHEZ, P. and Barberá, M. (2007): "Planificación aeroportuária y estratégias ambientales en Cataluña", in: Boletín de la A.G.E., nº45, pp. 99-121; [ Links ]

Submitted: 18.10.2011

Accepted: 25.11.2011