Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkTourism & Management Studies

versão impressa ISSN 2182-8458

TMStudies no.7 Faro dez. 2011

Modeling Domestic Tourism Demand in Galicia using the ARDL Approach

Modelando a procura turística doméstica na Galiza utilizando a abordagem ARDL

Manuel González-Gómez1; Marcos Álvarez-Díaz2 and Marisol Otero-Giráldez3

1Department of Applied Economics, University of Vigo mgonzalez@uvigo.es

2Department of Economics, University of Vigo

3Department of Applied Economics, University of Vigo

ABSTRACT

The aim of this paper is to find the most important socio-economic factors that statistically influence the domestic tourism demand to Galicia (North-west of Spain). For this purpose, we make use of the ARDL bounds testing cointegration approach (Pesaran et al., 2001). Once known the main influencing factors, we construct an econometric model using a general-tospecific ARDL modeling procedure. The findings allow us to quantify the impact of the influencing factors on the Galician domestic tourism demand. According to our results, the income elasticity of demand tends to be unitary; that is, an increase of 1 per cent in seasonally adjusted Industrial Production Index of the Spanish Economy produces a rise of around 1 per cent in the domestic tourism demand. Moreover, the Eastern vacations and the celebration of the Holy Year increase the tourism demand by around 11 per cent. Finally, the economic crisis and the differential of inflation between Galicia and the rest of Spain decrease the tourism demand.

KEYWORDS:: Domestic tourism demand modeling, ARDL approach, Bootstrapping, Galicia.

RESUMO

O turismo é um dos setores mais importantes para a economia da Galiza (Noroeste de Espanha). O objetivo do nosso trabalho é encontrar os mais importantes fatores socioeconómicos que, estatisticamente, influenciam a procura do turismo interno para a Galiza. Para este fim, fazemos uso da abordagem de cointegração de testes vinculados ARDL (Pesaran et al., 2001). Uma vez que os principais fatores que influenciam são conhecidos, construímos um modelo econométrico, utilizando um procedimento de modelagem ARDL do geral para o específico. Os coeficientes estimados do modelo permitem quantificar o impacto dos fatores que influenciam na procura do turismo doméstico galego. De acordo com nossos resultados, a elasticidade dos rendimentos da procura tende a ser unitária, ou seja, um aumento de 1 por cento dos rendimentos dos residentes espanhóis produz um aumento de cerca de 1 por cento na procura do turismo doméstico. Para além disso, as férias da Páscoa e a celebração do Ano Santo aumentam a procura turística em cerca de 11 por cento. Finalmente, a crise económica e o diferencial de inflação entre a Galiza e do resto da Espanha diminuem a procura turística em 7,5 por cento.

PALAVRAS-CHAVE: Modelagem de Demanda Interna de Turismo, Abordagem ARDL, Bootstrapping, Galiza.

1. Introduction

Galicia is a Spanish region located in the North-west corner of the Iberian Peninsula, right in the North border of Portugal. The economy is based on many diversified industries such as those related to the automotive sector, naval construction, clothing confection and fishing sector, among others. However, one of them, the tourism industry shows one of the most significant growth and is increasingly being considered one of the most important strategic economic sectors by the regional government, called "Xunta de Galicia". Since tourism policy has been transferred to the Autonomous Communities in Spain, the Xunta de Galicia has developed and revised policies with goal of increasing the contribution of the regional tourism industry to economic growth. In recent years the reports available for Galicia (Impactur Galicia 2007,2009) reflect the great relevance of the tourism industry for the Galician economy. According to these reports, tourism was estimated to contribute in 6,072 million of Euros to the Galician gross domestic product (GDP), a quantity that represents an increase of 4.6 percent over the previous year and a 10.9 percent of the regional GDP. Moreover, the strong backward and forward linkages with other industries not only have contributed to economic growth, but also have been an important factor in the creation of new jobs. Tourism is a labor-intensive sector that has a noticeably multiplier effect on the employment of the region. As indicated in the aforementioned study, for each 100 jobs directly generated in the tourism industry, it indirectly generates 51 jobs in other sectors. In general, the industry employs direct or indirectly around 132,000 people, a 10.3 percent of the total employment. Tourism is also an extremely important activity for the Galician regional government since it represents an important source of tax collection. Specifically, the taxation of the tourist activities implied revenues quantified in 1,130 million of Euros during 2007, amount that represented the 10.6 percent of the total tax collection of the regional government.

Despite the economic importance of tourism little work has been carried out on knowing what factors are the most relevant to explain domestic tourism demand to Galicia. A better knowledge of the demand for tourism could be of great assistance to the Xunta of Galicia in planning growth strategies for the tourist industry. To the best of our knowledge, Garín-Muñoz (2009) was the only study existing in the literature that analyzed the determinants of tourism to Galicia. She constructed a panel-data model and quantified the impacts of the determinants on international and domestic tourism demand. In general, most of the previous research on modeling assumes that tourism demand is predominantly influenced by socio-economic factors such as population, income, price level, substitute prices and marketing expenditures on promotional activities (Law and Au, 1999; Lim, 1999; Song and Witt, 2000).

A properly specified demand econometric model can help to discover the main factors affecting the domestic tourism demand to Galicia. For this goal, we construct a tourism demand model that includes socio-economic variables. The construction of this model allows us to estimate the impact of the main factors on the demand for tourism. This information can be relevant to derive reliable policy recommendations to the regional government in order to get an optimal use of the tourism-related resources. We centered our analysis in domestic demand because Galician tourism has a very large domestic component, and its economic contribution is much greater than international tourism. According to the Spanish Statistical Institute (INE), the residents in other regions of Spain were responsible of around 82 percent of the total arrivals and overnight stays in Galicia during the last decade. This fact explains why the Xunta de Galicia has been launching important advertisement campaigns focused on improving the tourism image of the region in the rest of Spain.

The econometric research is based on the bounds testing approach proposed by Pesaran et al. (2001). That is, we make use of an autoregressive distributed lag (ARDL) model in order to investigate whether a long-run equilibrium relationship exists between the domestic tourism demand to Galicia and its potential influencing factors. The ARDL bounds testing approach has been successfully applied in numerous fields, included tourism modeling (Narayan, 2004). If a long-run relationship was verified, we estimate the parameters of the ARDL model. Finally, we use the ARDL estimated coefficients to calculate the point estimates of the long-run effects of the explanatory variables on the domestic tourism demand to Galicia. We follow the recommendations of Song et al. (2010) and we construct confidence intervals for the long-run effects using the bootstrap technique (Efron and Tibshirani, 1998). Bootstrapping is a statistical, non-parametric and computationally intensive methodology that allows calculating empirically confidence intervals without assuming a specific distribution of the variable under study.

The remainder of this paper is structured as follows. Section 2 provides a description of the theoretical model and of the variables considered in this study. Section 3 details the bounds testing approach and the ARDL modeling procedure. Section 4 contains the main results and discussion, and Section 5 concludes.

2. Theoretical Model and Variables

We start our analysis assuming that the domestic tourism demand to Galicia in a specific month can be correctly represented by the model

;(1)

;(1)

is a linear functional form and

is a linear functional form and

is the disturbance term which is assumed to be an independent and identically distributed random variable

is the disturbance term which is assumed to be an independent and identically distributed random variable

is the variable to be explained and it represents a measure of the domestic tourism demand in a particular month; in this case, we consider the logarithm of the number of tourist nights spent in Galician hotels by Spanish residents. The vector (Pt,Tt,Ct,Et,Ht)contains the potential variables that could be relevant to explain domestic tourism demand. To be more precise, the explanatory variables are defined as it follows:

is the variable to be explained and it represents a measure of the domestic tourism demand in a particular month; in this case, we consider the logarithm of the number of tourist nights spent in Galician hotels by Spanish residents. The vector (Pt,Tt,Ct,Et,Ht)contains the potential variables that could be relevant to explain domestic tourism demand. To be more precise, the explanatory variables are defined as it follows:

Pt is the difference of the Consumer Price Index for tourism and hospitality services (CPIs) between Galicia and the rest of Spain. This variable is taken to be a proxy for the cost of tourism in Galicia.

Tt is the level of income in Spain. The better approximation to this variable is the Personal Disposable Income or the Gross Domestic Product. However, this information is not available with a monthly periodicity. In order to overcome this problem, we use the logarithm of the seasonally adjusted Industrial Production Index, which is a commonly-used proxy to measure income at a monthly level (González and Moral, 1995).

Ct is a dummy variable that captures the effect of the economic crisis. Specifically, the variable takes value one from January 2008.

Et is a dummy variable that takes value one if the Easter vacation falls in that month, and it takes value zero otherwise.

Ht is a dummy variable that collects the influence of the Holy Year in the years 1999, 2004 and 2010, corresponding to the sacred year when the festivity of Saint James the Apostle falls on Sunday. A Holy Year implies for Galicia the arrival of thousands of pilgrims to visit the tomb of the Apostle James. Moreover, during the Holy Year, the regional government organizes cultural events and international music concerts that attract the interest of many tourists.

The sample period object of analysis in our study covers the period from January 1999 to December 2010; therefore, the sample size has T=144 observations. The variables Yt and It were seasonally adjusted by moving average methods (Pierce, 1980). Moreover, a graphical analysis of these variables suggests that they are not stationary. The existence of non-stationary variables could imply a problem of spurious regression when we use the ordinary least square method to estimate the parameters of the model. An important exception is where the non stationary variables are integrated of order one, and the combinations of these I(1) variables are stationary, i.e. these non-stationary variables are cointegrated. If this was the case, the problem of spurious regression does not arise (Song et al., 2003).

The bounds testing Approach and the ARDL modeling procedure

In recent years, considerable attention has been paid to testing for the existence of short and long-run relationships between variables based on the use of different cointegration techniques (Engle and Granger, 1987; Johansen and Juselius, 1990). However, these methods can be applied only when the variables are integrated of the same order. This technical requirement puts a severe limitation on the traditional cointegration techniques. In order to overcome this restriction, Pesaran et al. (2001) suggested the ARDL testing bounds approach to test for the existence of a long-run relationship between variables, which is applicable irrespective of whether the underlying variables are I(0) or I(1) or a mixture of both. The test is relatively more efficient in small or finite sample data sizes than the traditional cointegration techniques. However, the procedure will not work in the presence of I(2) series (Oteng and Frimpong, 2006).

The ARDL approach to cointegration entails estimating the conditional error correction model (ECM)

where the symbol Δ represents the first-difference operator,

is the dependent variable,

is the dependent variable,  is the vector with the K explanatory variables, T is the tendency and

is the vector with the K explanatory variables, T is the tendency and

its associated parameter,

its associated parameter,

is the intersection parameter,

is the intersection parameter,

and

and

are the long-run parameters,

are the long-run parameters,

and

and

are the short-run parameters and, finally and as usual,

are the short-run parameters and, finally and as usual,

represents the disturbance term. The optimal number of lags (p) of the ECM is chosen using the Akaike Information Criterion (Akaike, 1973).

represents the disturbance term. The optimal number of lags (p) of the ECM is chosen using the Akaike Information Criterion (Akaike, 1973).

Following Pesaran et al. (2001), the testing procedure of a long run relationship between the variables are based on two alternative statistics. The first one is the F-test on the joint null hypothesis that the coefficients on the level variables lagged are jointly equal to zero

( ). The second statistic is an individual t-test on the lagged dependent variable

(

). The second statistic is an individual t-test on the lagged dependent variable

( ). These statistics have a non-standard distribution under the null hypothesis that no relationship exists between Yt and the vector Xt. However, Pesaran et al. (2001) derived their asymptotic distributions under the null and proposed critical value bounds, which allow us to accept or reject the null hypothesis. Therefore, if the statistics fall outside of their respective critical upper bound, then we reject the null hypothesis and we have evidence of a long-run relationship (indicating cointegration). If the statistics are below their respective critical lower bound, then we cannot reject the null hypothesis of no cointegration. Finally, if the statistic lies between the upper and lower critical bounds, then the inference is inconclusive.

). These statistics have a non-standard distribution under the null hypothesis that no relationship exists between Yt and the vector Xt. However, Pesaran et al. (2001) derived their asymptotic distributions under the null and proposed critical value bounds, which allow us to accept or reject the null hypothesis. Therefore, if the statistics fall outside of their respective critical upper bound, then we reject the null hypothesis and we have evidence of a long-run relationship (indicating cointegration). If the statistics are below their respective critical lower bound, then we cannot reject the null hypothesis of no cointegration. Finally, if the statistic lies between the upper and lower critical bounds, then the inference is inconclusive.

.

.

on the domestic tourism demand

on the domestic tourism demand

. According to Bardsen (1989), the long-run effects can be calculated by the expression

. According to Bardsen (1989), the long-run effects can be calculated by the expression

and

and

are the estimated long-run coefficients. However, several problems arise at this point. First,

are the estimated long-run coefficients. However, several problems arise at this point. First,

is a point estimation. That is, it only provides a single value to quantify the long-run effect, but it does not give information about the degree of variability associated to it (Song et al., 2010). The second problem is that we do not know anything about the statistical significance of

. A possible solution to solve these problems would be to construct confidence intervals for each

. An interval for each estimated long-run effect allows us to approximate its variability and to know its statistical significant: if the zero was contained in the interval, then the effect would not be statistically significant. However, it is not possible to use the basis of the traditional statistical inference to construct confidence intervals since

is a point estimation. That is, it only provides a single value to quantify the long-run effect, but it does not give information about the degree of variability associated to it (Song et al., 2010). The second problem is that we do not know anything about the statistical significance of

. A possible solution to solve these problems would be to construct confidence intervals for each

. An interval for each estimated long-run effect allows us to approximate its variability and to know its statistical significant: if the zero was contained in the interval, then the effect would not be statistically significant. However, it is not possible to use the basis of the traditional statistical inference to construct confidence intervals since

does not follow a normal distribution (it is estimated as a quotient of two normal variables). In order to overcome this problem, we construct confidence intervals based on a non-parametric method known as the bootstrap method (Efron and Tibshirani, 1998). Bootstrapping is a computationally intensive methodology that allows calculating empirically confidence intervals without assuming a specific distribution of

.

does not follow a normal distribution (it is estimated as a quotient of two normal variables). In order to overcome this problem, we construct confidence intervals based on a non-parametric method known as the bootstrap method (Efron and Tibshirani, 1998). Bootstrapping is a computationally intensive methodology that allows calculating empirically confidence intervals without assuming a specific distribution of

.

4. Empirical results

The ARDL bounds testing approach is employed in this study to investigate whether there is a long-run equilibrium relationship between the domestic tourism demand to Galicia and its potential influencing factors. However, we must check first that we are able to use the bounds testing approach; that is, we must verify that the variables object of analysis are not I(2). For this purpose, we apply the conventional Augmented Dickey-Fuller test (ADF) (Dickey and Fuller, 1981) to identify the order of integration of the variables. According to the results reported in Table 1, the variables are non-stationary in their levels, but they are stationary in first differences. Therefore, they are integrated of order one I(1), including the dependent variable. As a consequence, the ARDL approach can be used to determine the existence of a cointegration relationship between variables[i]. As we are working with monthly data and following the suggestion given in Pesaran and Pesaran (1997), we consider a maximum number of lags p =12in the ECM represented in the equation (2). As previously mentioned, the optimal number of lags (p) of the ECM is chosen using the Akaike Information Criterion.

Table 1: Results of the Augmented Dickey-Fuller test for unit root

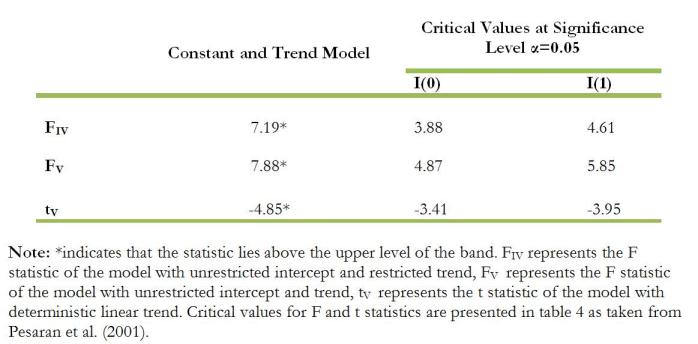

Pesaran et al. (2001) detail different scenarios to carry out the bounds testing approach, depending if the ECM has constant and/or trend. In our case, as both variables were statistically significant, we consider the F statistic of the model with unrestricted intercept and restricted trend (FIV), and with unrestricted intercepts and trend (FV). We also analyze the t-ratio calculated in a model with deterministic linear trend (tV). Table 2 shows the values of FIV, FV and tV, and the critical bounds for the different scenarios. In all cases, the tests lie above the critical upper bound. Therefore, the null hypotheses of no-cointegration are rejected implying in all cases the existence of a long run relationship between the variables. In other words, the vector of explanatory variables Xt =(Pt,It,Ct,Et,Ht) is relevant to explain the long-run dynamic of the domestic tourism demand to Galicia.

Table 2: Critical values and bounds test for cointendration

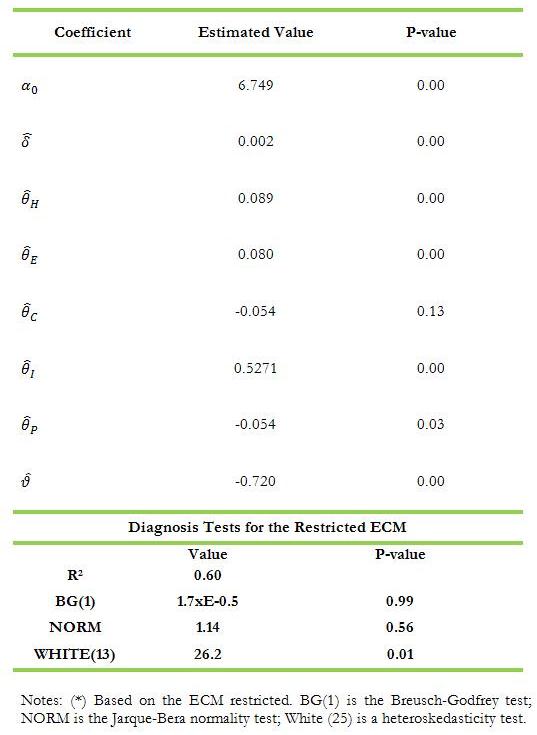

Once the long-run connection is verified, the next step is to construct a tourism demandmodel from the ECM specified in equation (2FOOT NOTE ), and using the general-to-specific modeling approach. Table 3 displays the estimated long-run coefficients ( ̂ and ̂), which are necessary to calculate the long-run effects.

Table 3: Long-run cointegration vector*

Table 3 also provides a battery of diagnosis tests that reveal the adequacy of the estimation procedure from an econometric point of view. The estimated model has a goodness of fit relatively high (R2=0.60), and passes all the diagnosis tests commonly used to detect problems of serial correlation and non-normality of the residuals. However, the White test reveals that there is a problem of heteroskedasticity. Actually, it is not a serious problem since it can be solved estimating the white hetoroskedasticity-consistent covariance matrix (White, 1980). The use of the consistent standard deviation has derived that the variable crisis (Ct) is not statistically significant at 10 per cent. However, we decided to maintain it in the model because it preserves the expected sign and it is statistical significance at 13 per cent. Moreover, the plots of the CUSUM and CUSUMSQ indicate the stability of both long and short run coefficients since the residuals lie within the upper and lower bounds of the critical values[ii].

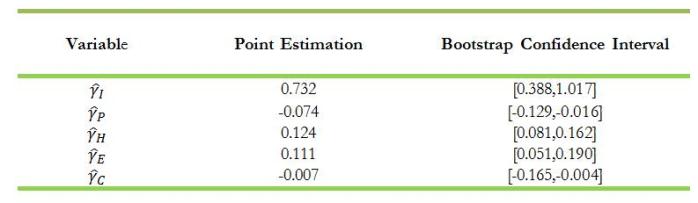

Having the estimated long-run coefficients of the ECM and using the expression (3), we are able to calculate de long-run effects of the explanatory variables on the domestic tourism demand to Galicia. Table 4 shows the estimated long-run effects and their associated bootstrap confidence intervals.

Table 4: Estimation of the long-run effects

According to these values: -. A one per cent increase in the Spanish industrial production will lead to a 0.732 per cent increase of the tourism demand to Galicia. The bootstrap confidence interval with a confidence level of 95 per cent for the income elasticity was (0.388, 1.017). It is worth noting that this estimation implies that the domestic tourism demand has unitary income elasticity. -. An increase of one point in the differential of inflation between Galicia and the rest of Spain will imply a reduction of 7.40 per cent in the demand. The associated bootstrap confidence interval was (-12.90, -1.6). -. If the Holy Year is celebrated, then the tourism demand increases a 12.40 per cent, with the true value located in an interval (8.10, 16.20). -. If Easter vacation falls on a specific month, the tourism demand in that month will increase 11.10 per cent. The bootstrap estimated confidence interval was (5.10, 19.00). -. Finally, and as it was expected, the economic crisis has affected negatively to the Galician tourism sector. Specifically, the tourism demand shrank by 7.41 per cent. The bootstrap confidence interval was (-16.72, -0.4).

In all cases, the confidence intervals constructed using the bootstrap technique does not include the zero. Therefore, we can affirm that the long-run effects are statistically significant at the 5 per cent.

4. CONCLUSIONS

This study attempts to model the domestic tourism demand to Galicia (Spain) using monthly socioeconomic data. We consider the ARDL bounds testing approach to verify the existence of a long-run relationship between the number of tourist nights spent in Galician hotels by Spanish residents, and a set of socio-economic factors such as income, the differential in the evolution of prices, the Holy Year, the Easter vacation and the economic crisis. Once checked the existence of a long-run connection between the variables, the next step was to use the ARDL model and the general-tospecific approach to construct a tourism demand model. The estimated long-run coefficients allow us to calculate the long-run effects of the socio-economic variables on the domestic tourism demand. The main findings of interest for professionals and policy makers can be summarized in the following points:

The socio-economic variables represented by the vector Xt= (PtItCtEtHt)are relevant to explain the long-run dynamic of the domestic tourism demand to Galicia. ·The income elasticity, that measures the reaction of the domestic tourism demand to a one percent increase in the Industrial Production Index of the Spanish economy in percentage, is unitary.

The celebration of the Holy Year has a considerable impact on tourism. The regional government should make a greater effort to promote the celebration of this event. Finally, this study represents only a first step that opens new possibilities of research. Further research will be needed in order to analyze not only the effect of socio-economic variables. Although these variables are indubitably relevant to explain demand for tourism, other factors which are not traditionally included in the tourism demand models could have also a significant influence such as climate, cultural values and natural attractions, some of which are difficult to quantify (Williams and Shaw, 1991).

References

AKAIKE, H. (1973), Information theory and an extension of the maximum likelihood principle, in Petrov, B. & Csake, F., (ed) Proceedings of the second international symposium on information theory, AkademiaiKiado, Budapest. [ Links ]

BARDSEN, G. (1989), Estimation of Long Run Coefficients in Error Correction Models, Oxford Bulletin of Economics and Statistics, 51 (3), 345-350. [ Links ]

DE VITA, G., AND ABBOTT, A. (2002), Are saving and investment cointegrated? An ARDL bounds testing approach, Economics Letters, 77 (2), 293-9. [ Links ]

DICKEY, D. A., AND FULLER, W.A. (1981), Likelihood ratio statistics for autoregressive time series with a unit root, Econometrica, 49, 1057–1072. [ Links ]

EFRON, B. AND TIBSHIRANI, R. J. (1998), An introduction to the bootstrap, Chapman & Hall, Boca Raton, Florida. [ Links ]

GARÍN-MUÑOZ, T. (2009), Tourism in Galicia: Foreign and domestic demand, Tourism Economics, 15 (4), 753-769. [ Links ]

GONZÁLEZ, P., AND MORAL P. (1995), An Analysis of the International Tourism Demand in Spain, International Journal of Forecasting, 11, 233-251. [ Links ]

HENDRY, D. F. (1993), Econometrics: Alchemy or science?Essays in Econometrics Methodology, Blackwell Publishers, Oxford. [ Links ]

IMPACTUR GALICIA 2007 (2009), www.exceltur.org. [ Links ]

LAW R., AU N. (1999), A neural network model to forecast Japanese demand for travel to Hong Kong,Tourism Management, 20, 89–97.

LIM, C. (1999), A Meta-Analytic Review of International Tourism Demand, Journal of Travel Research, 37, 273-289. [ Links ]

SONG, H., AND WITT S. F. (2000), Tourism Demand Modelling and Forecasting: ModernEconometric Approaches, Pergamon, Oxford. [ Links ]

NARAYAN, P. K. (2004), Fijis tourism demand: the ARDL approach to cointegration, Tourism Economics, 10 (2,) 193-206. [ Links ]

OTENG-ABAYIE, E. AND FRIMPONG J. (2006), Bounds Testing Approach to Cointegration: An Examination of Foreign Direct Investment Trade and Growth Relationships, American Journal of Applied Sciences, 3 (11), 2079-2085. [ Links ]

PESARA, M., SHIN Y., SMITH R. (2001), Bounds testing approaches to the analysis of level relationships, Journal of Applied Econometrics, 16, 289-326. [ Links ]

PIERCE, D. A. (1980), Data revisions with moving average seasonal adjustment procedures, Journal of Econometrics, 14, 95-114. [ Links ]

SONG, H., KIM, J., AND YANG, S. (2010), Confidence intervals fortourism demand elasticity, Annals of Tourism Research, 37 (2), 377–396. [ Links ]

WHITE, H. (1980), A heteroskedasticity-consistent variance matrix estimator and a direct test for heteroskedasticity, Econometrica, 48 (4), 817-838. [ Links ]

WILLIAMS, A., AND SHAW G. (1991), Tourism and Development: Introduction, in Williams, A., and Shaw, G., (eds.) Tourism and Economic Development: Western, European, Experiences (2nd ed.), Belhaven Press, London (1991), 1–12. [ Links ]

Submitted: 25.08.2011

Accepted: 26.10.2011

Notes

[i] The value added of the bounds testing procedure employed is that allows testing for cointegration when it is not known certainly whether the regressors are purely I(0), purely I(1) or mutually cointegrated (De Vita and Abbott, 2002)

[ii] The plots of CUSUM and CUSUMSQ are not reported in this study, but they can be sent by request.