Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkEconomia Global e Gestão

versão impressa ISSN 0873-7444

Economia Global e Gestão v.15 n.3 Lisboa dez. 2010

The role of China in the Portuguese speaking African countries: the case of Mozambique (Part I)

Fernanda Ilhéu

fernandailheu@iseg.utl.pt Doutora em Administração e Marketing, Universidade de Sevilha, Espanha. Docente no ISEG e coordenadora do ChinaLogus do CEGE/ISEG. PhD in Administration and Marketing, University of Seville, Spain. Professor at ISEG and coordinator of ChinaLogus of CEGE/ISEG.

ABSTRACT

Due to the Reform and Open Door Policies initiated in 1978, China recorded since then a fast sustainable economic growth, turning it into the worlds second largest economy. With an export oriented economic model, highly supported by Foreign Direct Investment, China became worlds number one exporter, after surpassing Germany in 2009. Presently China has the worlds largest foreign exchange currency funds, 50% of which are being applied in American bonds, while the remaining supports Chinese health and social security systems, Chinese banks solvability, internationalization of the Chinese economy, outward foreign direct investment (OFDI) and Chinese official foreign aid (ODA) to other developing countries. Although the Chinese OFDI fluxes are nowadays more oriented to mature economies, its bulk is mainly directed to partnerships with other developing countries like the African countries, and within those, the Chinese government identified one group strategically important to cooperate and invest, the Portuguese Speaking African Countries. These countries have high expectations on the Chinese investment and cooperation and our research questions are: (a) Should this investment be considered ODA or OFDI?; (b) How far can Chinese finance fluxes contribute to the development of these countries in terms of employment, exports, technology transfer?; (c) Is this investment seen as an opportunity or a threat by local people, is it fulfilling the created expectations or not? In this paper we concentrate our empirical research in Mozambiques case.

Keywords: China, Outward Foreign Direct Investment, Official Foreign Aid, Beijing Consensus, Portuguese Speaking African Countries, Mozambique.

O papel da China nos PALOP: o caso de Moçambique (Primeira Parte)

RESUMO

Devido às políticas de Reforma e Porta Aberta iniciadas em 1978, a China registou, desde essa altura, um rápido crescimento económico sustentado, tornando-a na segunda maior economia do mundo. Com um modelo económico orientado para a exportação, altamente suportado por Investimento Directo Externo, a China tornou-se no maior exportador mundial, depois de ultrapassar a Alemanha em 2009. Presentemente, a China tem a maior reserva do mundo de divisas estrangeiras, 50% aplicada em títulos do Tesouro americanos e o restante nos sistemas de saúde e segurança chineses, na solvabilidade dos bancos chineses, na internacionalização da economia chinesa, no investimento directo da China no exterior (IDENE) e na ajuda pública da China ao desenvolvimento de outros países (APED). Embora os fluxos de IDENE da China estejam hoje em dia mais virados para as economias maduras, a sua maior percentagem ainda se dirige a parcerias com outros países em desenvolvimento, como por exemplo os países africanos, e dentro destes o governo chinês identificou um grupo estrategicamente importante para cooperar e investir, os Países Africanos de Língua Oficial Portuguesa (PALOP). Estes países têm grandes expectativas no investimento e cooperação com a China e as questões que pesquisamos são: (a) Deve este investimento ser considerado IDENE ou APED?; (b) Até que ponto estes fluxos financeiros contribuem para o desenvolvimento desses países em termos de emprego, exportações, transferência de tecnologia?; (c) Este investimento é visto como uma ameaça ou uma oportunidade pela população local, está ele a corresponder às expectativas criadas ou não? Neste artigo iremos focar a nossa pesquisa no caso de Moçambique.

Palavras-chave: China, Investimento Directo da China no Exterior, Ajuda Pública da China ao Desenvolvimento, PALOP, Consenso de Pequim, Moçambique.

Introduction

Due to the Reform and Open Door Policies initiated in 1978, China recorded a fast sustainable economic growth, in the period of 1980-2009, with an estimated average GDP growth rate of 9.8%, turning China, in 2009, into the worlds second largest economy, just after USA. With an export oriented economic model, highly supported by Foreign Direct Investment (FDI) mostly from developed countries, China is since 2002 the most attractive developing country for FDI flows, both at short and long terms, becoming not only the worlds factory, but also its number one exporter, after surpassing Germany in 2009. With a sustainable current account surplus (US$ 253.3 billion in 2009) China has been able to achieve a foreign exchange reserve of US$ 2.3 trillion, the worlds largest reserve currency. Around 50% of this huge reserve is being applied in American bonds, while the remaining supports Chinese health and social security systems, Chinese banks solvability, internationalization of the Chinese economy, investment in geostrategic positioning to guarantee energy independence and foreign aid to other developing countries.

During 2008s global crisis, China was able to resist better than the major world economies, even benefiting from this downturn to implement policies to reduce its economic imbalances. One of these imbalances is the gap between Chinese Foreign Direct Investment (FDI) and Outward Foreign Direct Investment (OFDI) which is now progressively narrowing. In fact, in the near future, OFDI is expected even to be larger than FDI, Davis (2009) refer that China OFDI accounts for not much more than 1% of the global total, far below the countrys share of the world trade. However, this total is rising fast and the country will eventually become a major source of global FDI.

Mostly two types of Chinese OFDI can be distinguished: trade-oriented investment and resource–seeking investment. Governmental backing, including official developments assistance (ODA) has been crucial for the resource–seeking investment. Although the Chinese investment is nowadays more oriented to mature economies, its bulk is mainly directed to the other developing countries mainly to Asian countries, Latin America, and now also to African countries. Following the Beijing Consensus (non-interference in African affairs) , Chinese planners are pushing partnerships with African countries and within those, the Chinese government identified one strategic group worth to invest and cooperate with, the Portuguese Speaking African Countries which are linked through a network of language and culture between themselves and also to other geostrategic economic spaces; to Europe via Portugal, to Latin America via Brazil and to Asia via Macau.

FDI as a Foreign Markets Entry Mode

FDI is defined as an investment, involving a long-term relationship and reflects the objective of establishing a lasting interest and control by an individual or organization (foreign direct investor) of one country in an enterprise of a foreign country (Foreign Invested Enterprise - FIE). FDI implies that the investor exerts a significant degree of management and control in the FIE. This can be done by the transfer of capital flows to create a new venture (green field investment) but also by the acquisition of equity capital in an enterprise already existing in a foreign country. Reinvested earnings in the FIEs or short or long-terms loans between the foreign direct investor and the FIE is also considered FDI (UNCTAD, 2009).

OECD (2008) benchmarking definition of FDI, adds that the lasting interest implying a long-term relationship and a significant degree of influence and management and control requires at least the direct or indirect ownership of 10% of the voting power. Basically OECD defines FDI as an investment of an entity resident in one country that has acquired, either directly or indirectly at least 10% of the voting power of a corporation or equivalent for an incorporated company resident in another country. The entity that invests abroad can also contribute with other assets either than equity capital, like technology and production knowledge, that although being intangible assets can be evaluated and considered in the capital invested in the venture or are considered non-equity forms of investment.

Yan (2005) resumes FDI to two types of economic activities: the firms equity based investment, including the purchase of equity shares in foreign firms in foreign countries and the establishment of firms operations and management in foreign countries the equity based production.

International Business (IB) and Marketing theories, consider FDI (new ventures, joint ventures and acquisitions) as one entry mode into foreign markets, and in fact the one which reflects the higher degree of commitment to those market, allowing the higher involvement in the management and control of the ventures. Bradley (2002) refers that FDI in new ventures, joint ventures or acquisitions can only be considered when the firm is ready for heavy commitment of resources, accepts higher risks and has enlarged capacity of control.

Meyer (2004) considers that foreign investors establish their operations using three types of modes, normally classified as joint venture, acquisition and greenfield investments. Theoretically, the short term impact on the host country economy can vary with the type of entry mode, but there are not empirical evidences of this on long-term basis. This author concluded that greenfield investments creates new businesses and are normally seen as having positive impact on employment and domestic value added, but acquisitions can easily be seen with reserves by local population, governments and network partners. Joint ventures are welcomed if they bring mutual learning, knowledge transfer, risk sharing, and economies of scale in production and market distribution, as well as an increase in assets and resources.

The entry mode which represents the higher committed involvement in the international market is the FDI, with the direct ownership of 100% foreign capital, known in the literature as Wholly Owned Enterprise (WFOE), which represents the direct ownership of foreign based assembly manufacturing or services facilities (Terpstra and Sarathy, 1994; Kotler, 2003). Only in this entry mode, the firm has full control over the investment; it is fully independent to develop a long-term international market strategy, without conflict with local partners and can protect the company from local protectionism given to domestic companies. With this entry mode the firm acquires greater knowledge of the market and is able to appropriate local advantages without having to share it, and gets the possibility of integrating various national operations into a synergistic international system (Terpstra and Sarathy, 1994, p. 401).

Normally the company who chooses this entry mode might strengthen its image, and benefit from local governments goodwill, workers, customers, suppliers, distributors and the local society in general (Kotler, 2003).The main disadvantage of this entry mode is the large investment normally required, and the political or economic risks involved. The firm may also face higher exit barriers if the local government fear employment and economic lost with the firm withdraw from the country.

The firm may obtain wholly owned foreign production in two ways; developing its own facilities from zero or through the merger and acquisition of a foreign based firm. In some cases the structure of market can justify the Merger & Acquisitions (M&As) process as the only way to enter the market. One of the most common reasons to choose the M&As entry mode, is the pace of the company´s establishment and knowledge acquisition, local market experience, market share, labor force, institutional support, a network of suppliers, intermediaries and customers, contacts with local market operators and government, or acquiring a well-known brand with loyal clients, which allows the promptness of returns (Terpstra and Sarathy, 1994; Bradley, 2002).

But this can be a very expensive and risky way to enter the market due to the lack of transparency of the real market and poor finance situation of the local firm. According to Woodcock et al. (1994, p. 260) the acquisition entry mode has a cost associated with the risk of paying too much for the target firm, the cost of this risk is associated with the asymmetric information problem confronting the acquiring firm due to the firms inferior knowledge of the resources being purchased. Also the integration process can be problematic due to the difficulty of integrate two management teams with different languages, cultures and business practices, as concluded by these authors strategic implementation and organizational cultural differences make it very difficult for organizations to merge efficiently and effectively and also post-acquisitioned performance was negatively influenced by the two firms top managers divergent views of organizational culture (see p. 255).

So the foreign firm may not be able or want to buy a local operation and might prefer to build up a new venture from zero. The firm may want to introduce the latest technology and equipment, may want to avoid heritage problems, and may want to shape the local firm with its own culture practices and image (Terpstra and Sarathy, 1994). Smaller firms normally prefer new ventures, not only because they are frequently less expensive than acquisitions, but also the size of investment and firms commitment can be controlled and adjusted to the capacity of the foreign firm and market needs, being the expansion done accordingly with its market share growth and results (Bradley, 2002).

Also foreign investors may team up with local investors to create a joint venture company in which ownership control, risk, and market experience is shared. The foreign firm might lack market knowledge, finance, and physical or management resources to operate alone (Kotler, 2003), but other reason to form an international joint venture (IJV) can be to facilitate technology transfer (Bradley, 2002).We can observe that IJVs rise especially in difficult markets, and they are motivated by the desire of an international partner to have access to local market knowledge and culture as well as to local distribution channels, since accordingly with Bradley (2002, p.291) General knowledge of the local economy is the key contribution a local partner can make to an international firm seeking entry to a new foreign market.

In some countries, local conditions and/or government policies may guide foreign investors to joint local companies and create joint ventures in which they share capital, technology, management and markets. Many countries are known to impose or to have imposed legal restrictions to foreign ownership of local enterprises, some relaxed these restrictions on the 80´s, others did so later or are doing it now or didnt make it yet (Barkema and Vermeulen, 1998). Governments regulations can require local equity participation for example; India, China, Brazil and Thailand were successful in imposing the joint venture option to foreigners (Govindarajan & Gupta, 2001). Chinese government has oriented foreign investors to joint venture with local firms and in some sectors still imposes it (Vanhonaker and Pan, 1997).

Firms may prefer joint ventures as an entry mode in a culturally distant country, because joint ventures allow them to use the knowledge of the local partners, in local business practices, local institutions, distribution channels, customer preferences and so on (Kogut and Singh, 1988; Barkema and Vermeulen, 1998).

As for Terpstra and Sarathy (1994, p. 396) A joint venture is a foreign operation in which the international company has enough equity to have a voice in management but not enough to complete dominate the venture, and this might be the problem with this entry mode since dominant managerial control exercised by foreign partners is significantly and positively related to performance (Bradley, 2002, p. 294).

But performance is affected by conflicts between partners, and these conflicts easily happen, when there are different incompatible business operational routines, management practices, strategic views and expectations, and dominant management controls dont exist (Ding 1997) and since the cultural similarity between partners is a critical antecedent for IJV success. The greater the cultural similarity between IJV partners the better the IJV performance (Lin and Germain, 1998, p. 189), we can foresee that the greater the cultural disparity the worse the joint venture performance.

FDI Basic Motivations

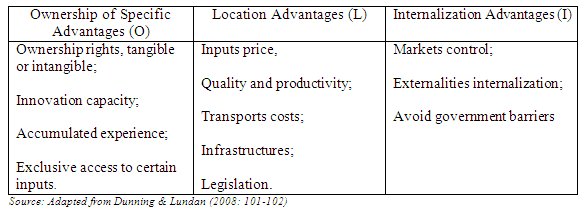

But FDI research for itself developed its own theories which can be seen through the perspective of an unified framework that attempts to incorporate the entry mode decision making of FDI, known as the Eclectic model or OLI (Ownership, Location, Internalization) model of Dunning as defended by Hill et al. (1990, p. 117) Dunning introduced a unified framework within which different factors can be placed and the relationship between them analyzed. The model of Dunning (1980, 1988), brought together aspects of industrial organization and location economics, but was particularly dependent on internalization analysis to explain FDI. The model introduces explicit considerations of ownership factors which are very close to the ideas of resources, skills and capacities in the Resources Based View models of multinationals enterprises (MNEs) or FDI strategic choices, (Fladmoe-Lindquist and Tallman, 1997). The Eclectic model identifies ownership-specific advantages, location-specific advantages and internalization-specific advantages as relevant factors for entry mode.

According to Dunning (1980) the ability of enterprises to acquire ownership advantages is related to specific endowments of their country of origin which is the base of their ownership advantages and of the countries they operate, as mentioned in p. 11, the possession of ownership advantages determines which firms will supply a particular foreign – market, whereas the pattern of location endowments explains whether the firm will supply that market by exports (trade) or by local production (non trade).

Ownership of specific advantages is the ownership of unique factors, meaning resources, skill capabilities developed in country of origin. Location advantages are linked to specific factors of a foreign country that could include cheap labor, superior production processes, local image, governmental trade barriers or others, which justify to undertake production in that country in order to obtain new competitive advantages, that can be internally exploited, through complementary resources of the firm like an international distribution network, or finance capability. Internalization advantages refer to benefits of retaining assets and skills in the firm, market controls among others, Table 1.

Table 1 – Some OLI Paradigm Advantages

Dunning (1977, 1993) suggests three basic motivations to justify FDI, influencing also its location: foreign market-seeking, efficiency (cost reduction) seeking and resource-seeking (including strategic-asset-seeking). Market-seeking FDI is frequently used by firms to gain access to distribution networks and to enhance exports. Efficiency-seeking FDI normally occurrs when firms seek lower-cost locations for operations or seek high technologic operation centers and resources-seeking FDI is practiced by firms who need to acquire or guarantee the supply of raw-materials, energy and other kind of assets like knowledge and experience in a market, patents or famous brands.

This theoretical approach mostly done through the perspective of IB and marketing theories, can be complemented with economic development researches, which looks for answers to the questions: what is the relation between economic development of one country and its inward and outward foreign investment and what is the contribution for the economic development of the host country of the inward foreign investment?

Relationship between Economic Development and FDI and OFDI

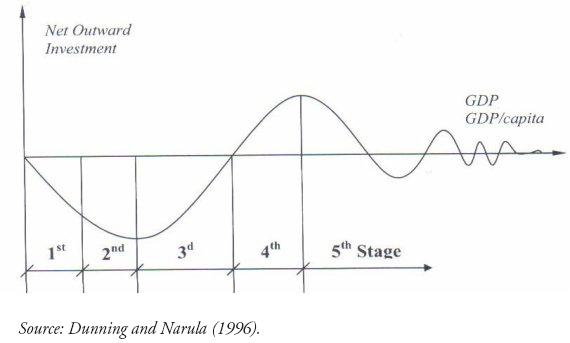

A widely used framework for researching the relationship between inward FDI from foreign firms, outward foreign investment of domestic firms and economic development of the host country is the Investment Development Path (IDP) proposed by Dunning (1981) and further developed mainly by Dunning and Narula (1996) and Durán and Úbeda (2001, 2005). According to these researchers, IDP is a dynamic sequential model, with 5 stages of economic development, analyzed in terms of GDP or GDP per capita that relates a country net outward direct investment (NOI) with its economic development stage. This progressive stages starts with a 1st stage where the country is a net receiver of inward FDI and goes to the 5th stage where the country is a net outward investor (Figure 1).

Figure 1 - Model - Investment Development Path Stages

An empirical study of Mendonça et al. (2009) confirmed this model, showing a relationship between GDP per capita and NOI – the results were obtained in a sample comprising USA, Japan and 23 EU countries. Durán and Úbeda (2005) concluded, that the main variables that defines countries in the 1st, 2nd and 3rd stages (less developed economies) is inward FDI, although outward FDI and NOI can be verified in a group of these countries, they demonstrated that 4th stage countries are focusing outward FDI, while the 5th stage countries are characterized by a positive NOI.

Dunning et al. (2001) developed the IDP model, considering countries with different types of products and industries, but belonging to the same development stages (based mostly in the GDP per capita, in terms of 1994 US$ values), being these stages the main determinants of the verified inward and outward investment flows. In the Stage 1 of IDP – pre-industrial stage (GDP per capita below US$1000) the country receives a small amount of inward FDI, due to insufficient market size and poor infrastructures, and has insignificant outward FDI, explained by their firms weak O-advantages. The Stage 2 is characterized by a GDP per capita between US$1000-$3000, in which economic growth, infrastructures projects development and enlarged market size, attracts market-seeking and resource-seeking FDI. Some OFDI can also begin as a result of the internationalization of domestic firms, but in this stage the country is a net recipient of FDI. In the Stage 3 with GDP per capita from $3000 to $10 000, improvements in L-advantages go on being registered and the country continues to attract significant amounts of FDI. Domestic companies begin to develop O-advantages, and their internationalization process explain the exploitation of their own specific assets in foreign markets, increasing the amount of OFDI flows, but the country remains a net recipient of FDI. At the 4th Stage GDP per capita exceeds $10 000 and the country is normally characterized by being a net outward investor, with OFDI increasing faster than FDI. Finally in 5th Stage the country is characterized by having high living standards and advanced technology, becoming major importer and exporter of FDI, and the FDI and OFDI are balanced.

Chinese Economic Growth and Evolution of Chinese OFDI Policy

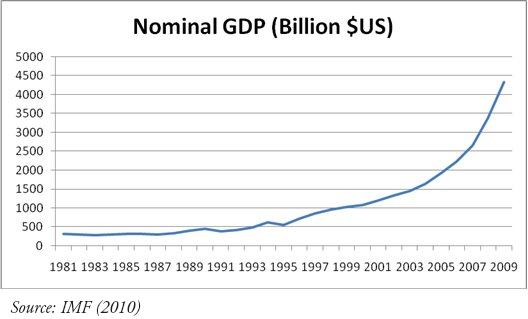

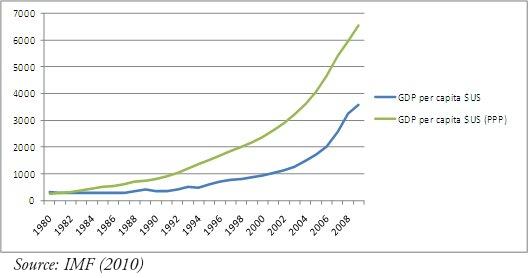

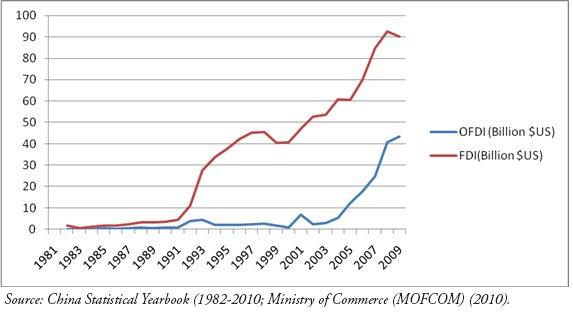

Statistical observation confirms a relationship between the evolution of China economic growth and inward and outward FDI see Figures 2, 3 and 4. According to the classification of Dunning et al. (2001), China is now on Stage 2 on the bridge to Stage 3, remaining an important recipient of FDI but increasing substantively and at a very fast pace the amount of OFDI, although still being a net recipient of FDI.

Fig: 2 – Chinese GDP growth

Fig: 3 – Evolution of Chinese GDP per capita (nominal and PPP)

Fig: 4 – Evolution of Chinese Inward and Outward Investment

IDP pattern varies significantly across developing countries but the case of China is so different that Dunning et al. (2001) and Liu et al. (2005) among others, consider GDP per capita insufficient to explain Chinese OFDI.

Liu et al. (2005) researched three supplementary variables (the local investment in human resources, the exports and the inward FDI) and their conclusions postulate, that the increase in GDP per capita and the investment in human resources are positively correlated with Chinese outward investment, but the exports effects in OFDI are ambiguous, however they found a significant interaction between inward FDI and OFDI. Other important conclusion is that Chinas OFDI seems to be consistent with an economy at Chinas level of economic development; the tested model suggests that policies specially directed to OFDI may be unnecessary, since OFDI seems to follow economic development automatically. The conclusions of Gao (2008) dont differ most from the ones of Liu et al. (2005). He found that GDP per capita indirectly influence Chinas OFDI and proved that the outward investment of China is directly influenced by the overseas network, knowledge building (investment in R&D) and market openness (inward FDI).

Buckley et al. (2007) researched if OFDI from China requires a special theory within Dunning general theory, calling our attention for three potential arguments: capital market imperfections, special ownership advantages of Chinese MNEs and institutional factors. Capital imperfection could be found in China, as State Owned Enterprises (SOEs) can access capital below market rates, inefficient banking system may make soft loans available to OFDI as a policy, conglomerate firms may be funded with subsidies (state-sponsored soft loans), family owned firms can obtain cheap capital from family members. Chinese low cost capital for Chinese firms mostly SOEs made available by market imperfections can explain that M&As is often chosen as the mode of entering a new market, and the perception of risk is not as rigorous as it is for firms of industrialized economies. This turns on to be an ownership advantage of Chinese MNEs, being others the flexibility and the networking skills of the Chinese Diaspora. State direct or indirect influence over these firms, is going to drive the decision of outward investment and its location pattern, according to criteria that are not profit maximization as in the general theory.

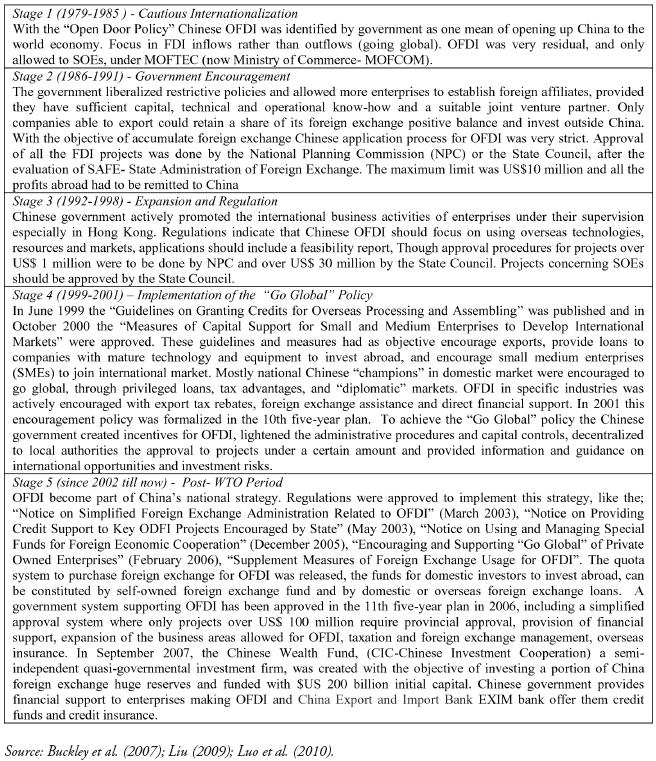

Although policies especially directed to OFDI might not be necessary as theories referred above, the fact is that governments in emerging economies such as India, China and Brazil actively encourage their domestic enterprises to go global (WIR, 2009). A good example is China, that in the last 30 years emerge from a marginal to an important source of OFDI (Luo et al., 2010), its domestic government policy was the main determinant of Chinese OFDI on the beginning of the Chinese internationalization, and after 2001 with the implementation of the Go Global policy, when the controls on outward investments start being steadily relaxed and at the same time Chinese companies begin to be encouraged to invest outward following its own commercial strategies. Through the implementation process of this policy the Chinese government passed from regulator to supporter of OFDI and we can even say to promoter within certain drivers (Table 2).

Table 2 – Key Stages of the Chinese Outward Foreign Direct Investment

Theoretical Conclusions

Chinese OFDI does not oppose to Dunning´s general theory but cannot be explained only by it even after considering supplementary variables, such as the local investment in human resources, the exports and the inward FDI, the overseas network and knowledge building.

Buckley et al. (2007) researched if OFDI from China requires a special theory within Dunning theoretical framework, calling our attention for three potential arguments; capital market imperfections, special ownership advantages of Chinese MNEs and institutional factors.

Capital imperfections could be found in China, as SOEs can access capital below market rates. Chinese low cost capital for Chinese firms mostly SOEs made available by market imperfections may explain that M&As is often chosen as entering mode into a new market, and the perception of risk is not as rigorous as it is for firms of industrialized economies. This turns on to be an ownership advantage of Chinese MNEs, being others the flexibility and the networking skills of the Chinese Diaspora. State direct or indirect influence over these firms, is going to drive their decision of outward investment and its location pattern with criterions that are not profit maximization as in the general theory.

The conclusion is that Chinese government actively encourages their domestic enterprises to go global with the implementation of the Go Global policy, being Chinese companies encouraged to invest outward following its own commercial strategies. In last 30 years Chinese government passed from regulator to supporter of OFDI and we can even say to promoter within certain drivers.

References

BARKEMA, H. G. & VERMEULEN, F. (1998), « International expansion through start-up or acquisition: a learning perspective», Academy of Management Journal, vol. 41, no. 1, pp.7-26.

BRADLEY, F. (2002), International Marketing Strategy, 4th, FT Prentice Hall.

BUCKLEY, P.J.; CLEGG, J.; CROSS, A. R.; LIU, X.; VOSS, H. & ZHENG, P. (2007), The determinants of Chinese outward foreign direct investment. Journal of International Business Studies, 38(4), pp. 499-518.

China Statistical Yearbook , 1982-2010.

DAVIS, K. (2009), «While global FDI falls, Chinas outward FDI doubles». Columbia FDI in Perspectives – Perspectives on topical foreign direct investment issues, Vale Columbia Center on Sustainable Investment, 5 May.

DING, D. Z. (1997), «Control, conflict, and performance: a study of U.S.-Chinese joint-ventures». Journal of International Marketing, 5(3), pp.31-45.

DUNNING, J.H. (1977), «Trade, location of economic activity and the MNE: a search for an eclectic approach» In B. Ohin; P. O. Hessalbom and P. M.Wijkman (Eds.), The International Allocation for Economic Activity, P.M., Macmillan, London.

DUNNING, J.H. (1980), «Toward an eclectic theory of international production: some empirical tests». Journal of International Business Studies, 11(1), pp. 9-31.

DUNNING, J.H. (1981), «Explaining the international direct investment position of countries: toward a dynamic and development approach». Weltwirtschaftliches Archive, 117(5), pp.30-64.

DUNNING, J. H. (1988), «The eclectic paradigm of international production, a restatement and some possible extensions». Journal of International Business Studies, Spring, pp.1-31.

DUNNING, J.H. (1993), Multinational Enterprises and the Global Economy, Addison Wesley Publishing Company, England.

DUNNING, J.H. & NARULA, R. (1996), «The investment development path revisited: some emerging issues». In J.H. Dunning and R. Narula (Eds.), Foreign Direct Investment and Governance. Routledge, London.

DUNNING, J.H.; KIM, C. & LIN, J. (2001), «Incorporating trade into the investment development path: a case study of Korea and Taiwan». Oxford Development Studies, 29(2), pp. 145-154.

DUNNING, J. & LUNDAN, S. M. LUNDAN (2008), Multinational Enterprises and the Global Economy. 2nd ed., Cornwall UK, Edward Elgar.

DURÁN, J.J. & ÚBEDA, F. (2001), «The investment path: a new methodological approach and some theoretical issues». Transnational Corporations, 10(2), pp.1-34.

DURÁN, J.J. & ÚBEDA, F. (2005), «The investment development path of newly developed countries». International Journal of the Economics of Business, 12(1), pp.123-137.

FLADMOE-LINDQUIST, K. & TALLMAN, S. (1997), «Strategic management in a global economy». In H.V. Wortzel and L. H. Wortzel (Eds.), John Wiley and Sons, Inc., pp.149-167.

GAO, L. (2008), «Determinants of Chinas outward foreign direct investment». Paper presented in CEA Conference: Chinas Three Decades of Economic Reform (1978-2008), University of Cambridge, UK.

GOVINDARAJAN, V. & GUPTA, A. (2001), The Quest for Global Dominance. Jossey Bass.

HILL, C. W.L.; HWANG, P. & KIM, W. C. (1990), «An eclectic theory of the choice of international entry mode». Strategic Management Journal, vol. II, pp.117-128.

IMF – International Monetary Fund (2010), World Economic Outlook. (April), www.imf.org

KOGUT, B. & SINGH, H. (1988), «The effect of national culture on the choice of entry mode». Journal of International Business Studies, 19, pp. 411-432.

KOTLER, P. (2003), Marketing Management. 11th ed., Prentice-Hall International.

Jornal Tribuna de Macau (2009). www.jtm.com.mo.

LIN, X. & GERMAIN, R. (1998), «Sustaining satisfactory joint-venture relationship: the role of conflict resolution strategy». Journal of International Business Studies, 29, (First Quarter), pp. 179-196.

LIU, X.; BUCK, T. & SHU, C (2005), «Chinese economic development, the next stage: outward FDI?». International Business Review, 14(1), pp. 97-115.

LIU, H. (2009), Chinese Business; Landscapes and Strategies. Routledge.

LUO, Y.; XUE, Q. & HAN, B. (2010), « How emerging market governments promote outward FDI: experience from China». Journal of World Business, 45, pp. 68-79.

MENDONÇA, A.; PASSOS, J. & FONSECA, M. (2009), « The investment path hypothesis: a panel data approach for Portugal and the cohesion countries, 1990-2007». Paper presented in the 3rd National Congress of Portuguese Economists in Funchal, Madeira.

MEYER, K. (2004), «Perspectives on multinational enterprises in emerging economies». Journal of International Business Studies, 35, pp. 259-276. [ Links ]

MOFCOM (2008), Statistical Bulletin of Chinas Outward Foreign Direct Investment.

MOFCOM (2010), Ministry of Commerce the Peoples Republic of China «Foreign trade and investment statistics». www.english.mofcom.gov.cn.

MOFCOM (2010), Statistical Yearbook 1982-2010.

OECD (2008), «Investment policy reviews China. China outward direct investment». www.oecd.org.

OECD (2008), «Benchmark definition of foreign direct investment», 4th ed. www.oecd.org.

TERPSTRA, V. & SARATHY, R. (1994), International Marketing, 6th ed., The Dryden Press, Orlando.

UNCTAD (2009), World Investment Report.

UNCTAD (2009), WIR – World Investment Report, Transnational Corporations, Agriculture Production and Development.

VANHONAKER, W. & PAN, Y. (1997), «The impact of national culture, business scope, and geographic location on joint-venture operations in China». Journal of International Marketing, 5(3), pp. 11-30.

WOODCOCK, C.P.; BEAMISH, P. W. & MAKINO, S. (1994), «Ownership-based entry mode strategies and international performance», Journal of International Business Studies, Second Quarter, pp. 253-273.

YAN, Y. (2005), Foreign Investment and Cooperate Governance in China. Palgrave, Macmillan, New York.